| BE | Accounts Receivable | Subsidiary account | DEBIT | Accounts Payable | Subsidiary account | CREDIT |

|---|---|---|---|---|---|---|

| A | A’s AR account | C’s local customer ID | 300 | A’s AP account | B’s local vendor ID | 100 |

| B | B’s AR account | A’s local customer ID | 100 | B’s AP account | C’s local vendor ID | 200 |

| C | C’s AR account | B’s local customer ID | 200 | C’s AP account | A’s local vendor ID | 300 |

Journal entries reflecting cycle’s reduction for those businesses may look like (POST REF column is hidden):

| BE | Date | Ledger account | Subsidiary account | ACCOUNT TITLES AND EXPLANATION | DEBIT | CREDIT | |

|---|---|---|---|---|---|---|---|

| A | YYYYMMDD | AP acct No. | B’s vendor ID | AP for B | 100 | ||

| AR acct No. | C’s customer ID | AR for C | 100 | ||||

| ARMO:DT= 1,CR= 1 | |||||||

| B | YYYYMMDD | AP acct No. | C’s vendor ID | AP for C | 100 | ||

| AR acct No. | A’s customer ID | AR for A | 100 | ||||

| ARMO:DT= 1,CR= 1 | |||||||

| C | YYYYMMDD | AP acct No. | A’s vendor ID | AP for A | 100 | ||

| AR acct No. | B’s customer ID | AR for B | 100 | ||||

| ARMO:DT= 1,CR= 1 |

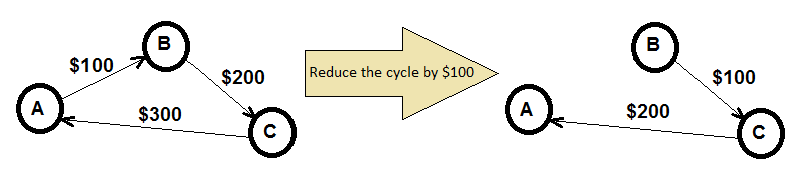

Explanations beginning with “ARMO:” show cycles’ numbers in which DT and CR values were accumulated. DT/CR values reduce correponding AP/AR balances when transactions are posted--see reduced cycle on the right (zeroed edge not shown) and the table below.

| BE | Accounts Receivable | Subsidiary account | DEBIT | Accounts Payable | Subsidiary account | CREDIT |

|---|---|---|---|---|---|---|

| A | A’s AR account | C’s local customer ID | 200 | A’s AP account | B’s local vendor ID | 0 |

| B | B’s AR account | A’s local customer ID | 0 | B’s AP account | C’s local vendor ID | 100 |

| C | C’s AR account | B’s local customer ID | 100 | C’s AP account | A’s local vendor ID | 200 |

Introduced here ARMO transaction reduces all AP and AR without any money transfers.

In case with large amount of BEs and long cycles of obligations their possible reduction may be accomplished by means of an information system developed for that purpose. This example displays a result generated by the System prototype.